In the face of more regional bank crashes and numerous worries about the economy, the stock market continued to hang tough. In fact, stocks have rallied late for two consecutive weeks.

- Stocks continue to defy the negative sentiment and look ready to move higher.

- A common narrative is only five stocks are pulling the entire market higher, but this isn’t true.

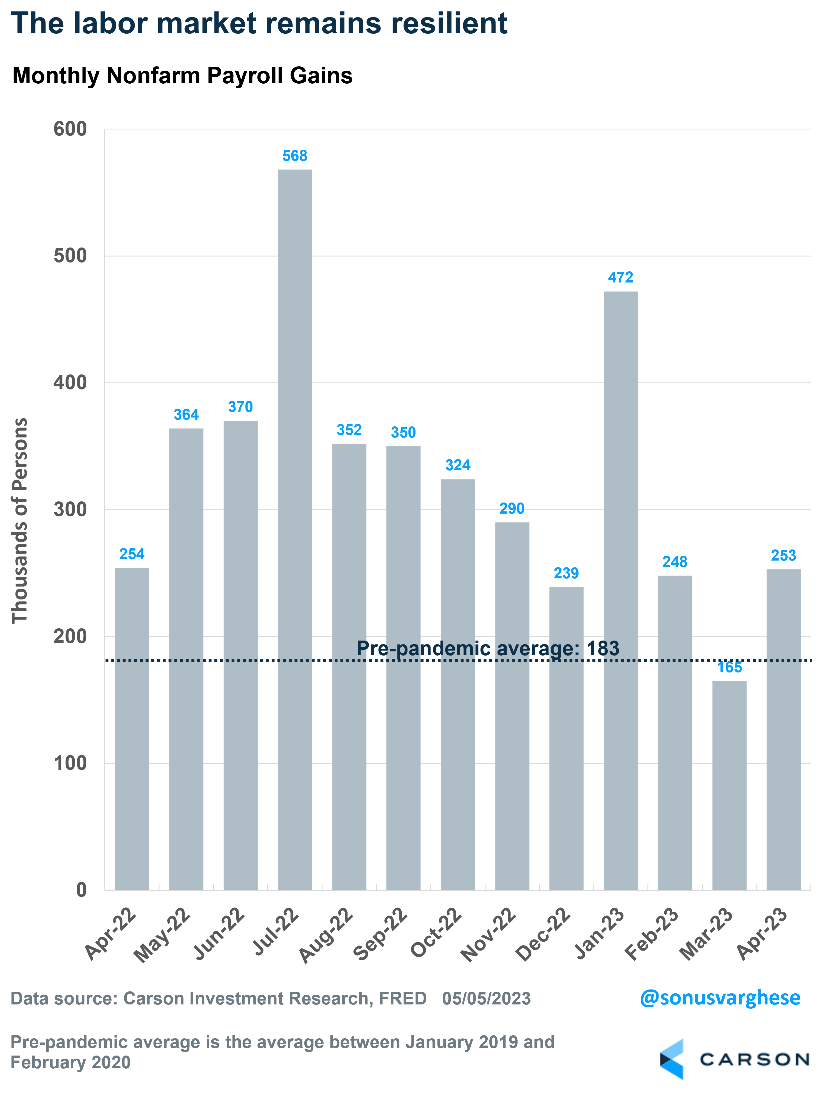

- April employment data suggests the economy is healthy.

- The economy created 253,000 jobs in April, above expectations of 179,000.

- The unemployment rate is at 3.4%, the lowest it has been since 1953.

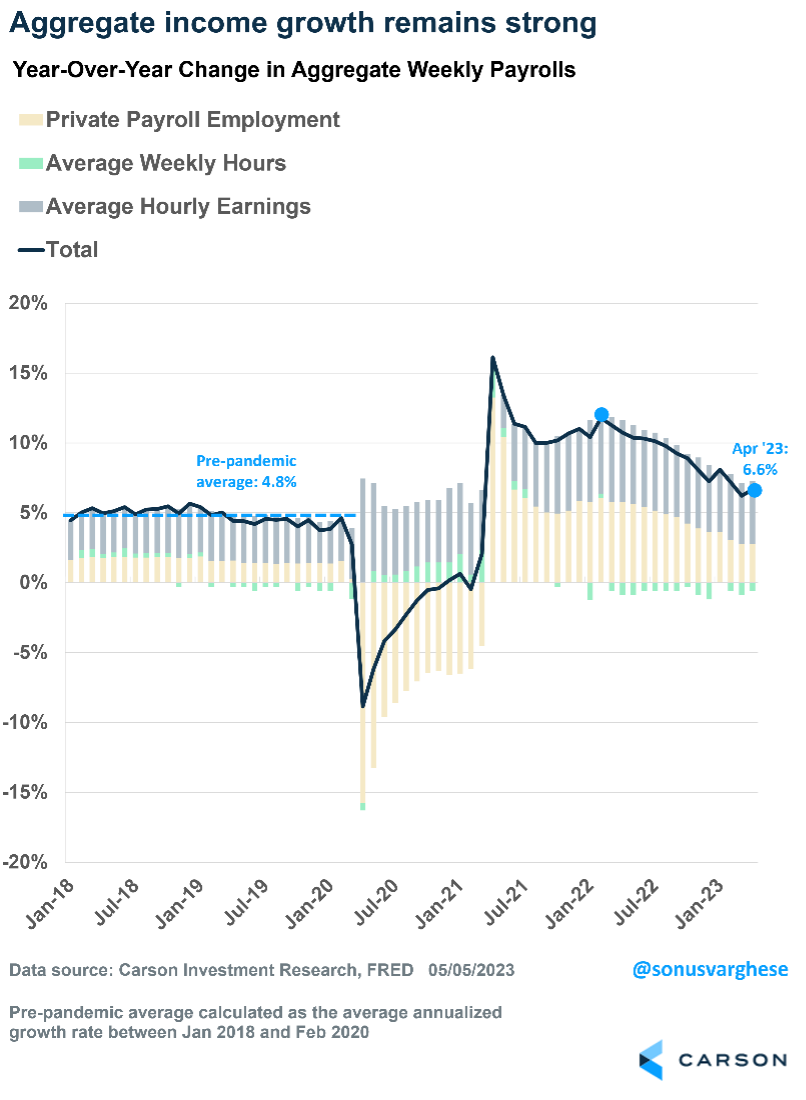

- Aggregate incomes across the entire economy are growing faster than inflation, which is good news for consumption.

- The Federal Reserve raised rates by 0.25% at its May meeting.

- Fed officials are likely to pause rate hikes, but the strong economy suggests they will not be cutting rates soon.

In what might come as a surprise for many investors, the S&P 500 is virtually flat over the past year. Despite countless negative events — record high inflation, a bond market crash, the most aggressive Fed policy in 40 years, the war in Ukraine, lockdowns in China, the second and third largest bank failures ever, an earnings recession, a mortgage market crash, and many more negative events — stocks are flat. To us, that’s a win and shows how resilient the economy and markets have been. Going forward, the 4,200 level on the S&P 500 is significant. As the chart below shows, this area has proved to be troublesome in the past. But we continue to expect higher prices in 2023 and think this level will give way soon.

Many Stocks Are Going Up

A common concern is that a handful of large stocks account for most of the stock market’s gains. This is a bearish notion as it suggests there have been weak underpinnings to the rally since October. A bull market survives with broad participation.

It has been widely reported that the largest two stocks in the S&P 500 (Microsoft and Apple) represent close to 40% of the rally this year, and the FAANG companies — Meta (formerly Facebook), Amazon, Apple, Nvidia, and Alphabet (formerly Google) — account for about 80% of the year-to-date gains.

However, this is perfectly normal. The best stocks always account for most of the gains. It’s similar to sports where the best players account for most of the points or great plays. This isn’t odd or nefarious.

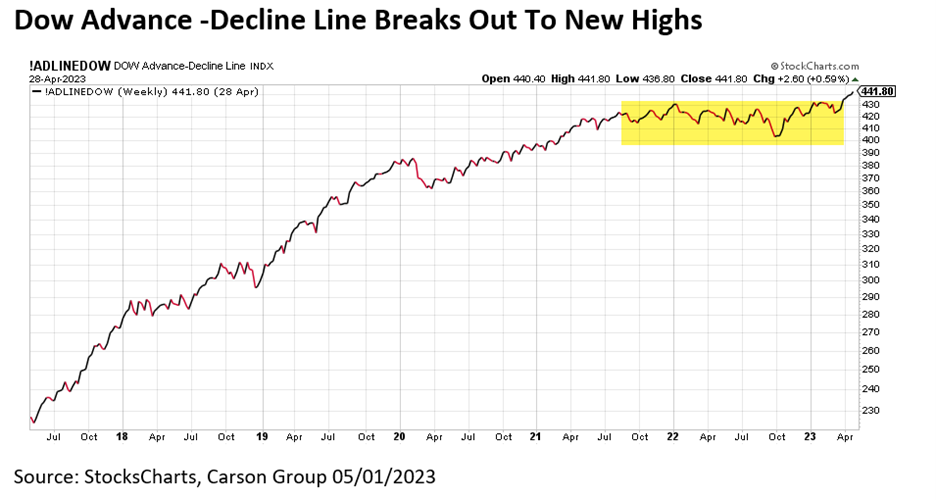

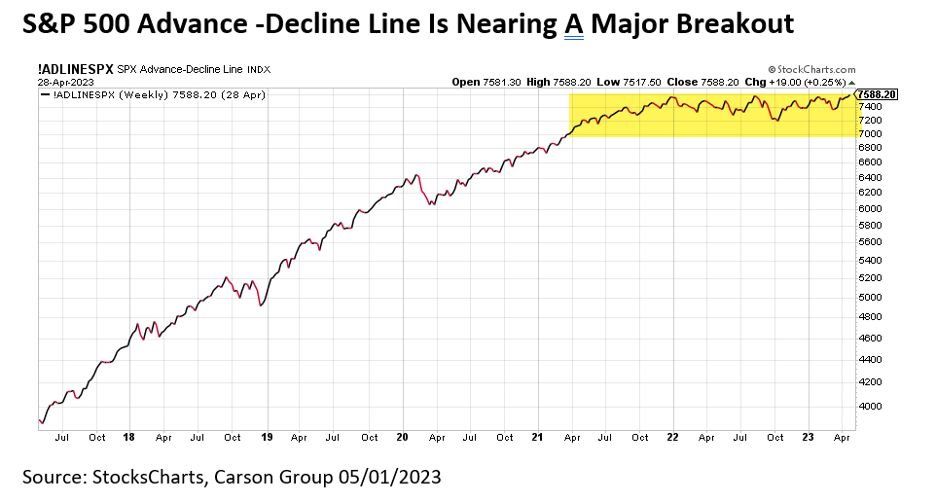

What’s the easiest way to show that more than a few stocks are rising? I like to use advance-decline (A/D) lines for this purpose. An A/D line is simply a cumulative total of how many stocks went up or down each day. Throughout the market’s history, A/D lines have broken out to new highs before the indexes, while they also break down well ahead of actual price. This is one of the best ways to see what is really happening under the surface.

The Dow A/D line recently reached new highs after consolidating for more than a year. With the Dow about 6% away from new highs, this is a clue that the nearly 125-year-old index may be following the A/D line to new highs sooner than later.

The S&P 500 A/D line shows another potentially bullish scenario. This one hasn’t quite broken out to new highs, but it is extremely close. Take note how this has trended sideways for the duration of the recent bear market, implying the tailwind for a bull market wasn’t happening. Should this break out, as we expect, it could suggest continued strength through 2023 and potentially beyond.

Data Suggests the Economy Is Healthy

If you were worried about a sudden stop for the economy on the back of a banking crisis, fear not. The April employment data suggests the economy is doing just fine, and perhaps more than fine. Of course, the banking crisis is a problem. Banks are tightening credit availability, but that will likely be a slow-moving adverse force on the economy.

Let’s get to the numbers.

The economy created 253,000 jobs in April, well above economists’ expectations for a 179,000 increase. Payroll numbers in February and March were less than what was originally reported, as they were revised down by 149,000. So, job growth in the first quarter was slightly weaker than originally thought.

But here’s the big picture: The economy has created more than 1.1 million jobs in the first four months of 2023. Even excluding January, the last three months have averaged 222,000 jobs. That’s well above the pre-pandemic average of 183,000, which was a very strong pace.

A Historically Strong Labor Market

Any skepticism of the job creation numbers washes away with the unemployment rate, which fell to 3.4%. That’s the lowest level since 1969!

What Does This Mean for the Federal Reserve?

The Fed’s aggressive rate-hike campaign to fight inflation appears close to an end. The Fed has raised rates by 5%, including the latest 0.25% increase implemented last week. The federal funds rate is now in the 5-5.25% range, which was the highest point it reached during the mid-2000s economic expansion.

The rate hike in May was expected, but more welcome was the fact that the Fed didn’t think “additional policy firming may be appropriate.” While this was not an explicit signal that Fed officials are pausing, it indicated they will be more data dependent. Fed Chair Jerome Powell explicitly referenced this in his comments about the future direction of policy, saying it will be assessed based on incoming data, including employment and inflation. The Fed has done a lot — and officials believe the economy is yet to reflect the full impact.

The April payroll report suggests the labor market remains strong, which means the Fed is unlikely to cut interest rates any time soon.

Average hourly earnings accelerated in April, rising at a 5.9% annualized pace for all private workers. These numbers can be noisy, so it helps to look at an average. But even that is running high. Average hourly earnings have been growing at a 4.2% annualized pace over the past three months, and they are up 4.4% over the past year. Pretty steady, but that also means the Fed will remain concerned about inflation. In the Fed model, strong wage growth is likely to keep underlying inflation elevated.

The biggest reason that the employment picture matters is consumption makes up 70% of the economy. And consumption is driven by income. Overall income across the entire economy is dependent on three factors:

- Employment growth (strong)

- Wage growth (strong, but maybe too strong for the Fed)

- Hours worked (steady)

Multiplying these factors adds up to overall income growth across the U.S. economy, which is up 6.6% over the past year. It’s down from about 12% in February 2022, but still above pre-pandemic levels.

Even better news — income growth is running above inflation, which is up about 5% over the past year — and energy and food prices continue to fall. That means people have more money in their pockets, which is positive for the economy.

In summary, there’s no sign of a slowdown yet. While that’s encouraging news for the economy, it also means the Fed will probably keep interest rates higher for longer.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case # 01757879